Trends and Developments within the Fast-Service channel in the Netherlands

Reading time: 7 min

The fast-service channel in the Netherlands is undergoing significant transformations. After growing over the past years, we now see a change in the dynamics of the market. In this article, we will analyse the evolution of the outlet numbers, have a look at the regional disparities, examine the differences between chain and independent outlets, and conclude with insights from our Market Monitor.

This article will focus on the following segments:

• Fast food – Salad/pasta/noodles/sushi

• Fast food – Shawarma/Kebab

• Fast food – Snack & fries

• Restaurants – Fast casual

Market Overview: Growth and Decline

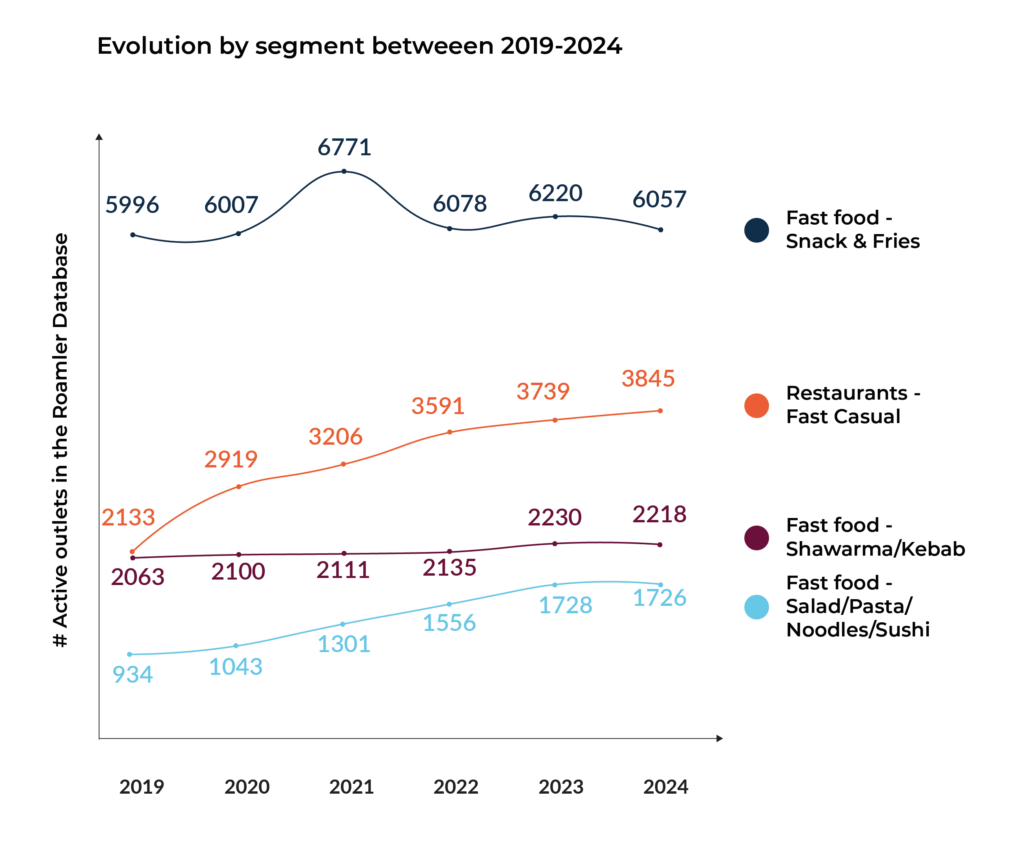

Over the past five years, the fast-service market in the Netherlands has witnessed growth across all the 4 segments analyzed. This is especially true for fast-casual restaurants and outlets serving other types of fast food like salads, pasta, noodles, or sushi (+85% between 2019 and 2023). Snack bars experienced a significant peak during the pandemic (+12% between 2020 and 2021).

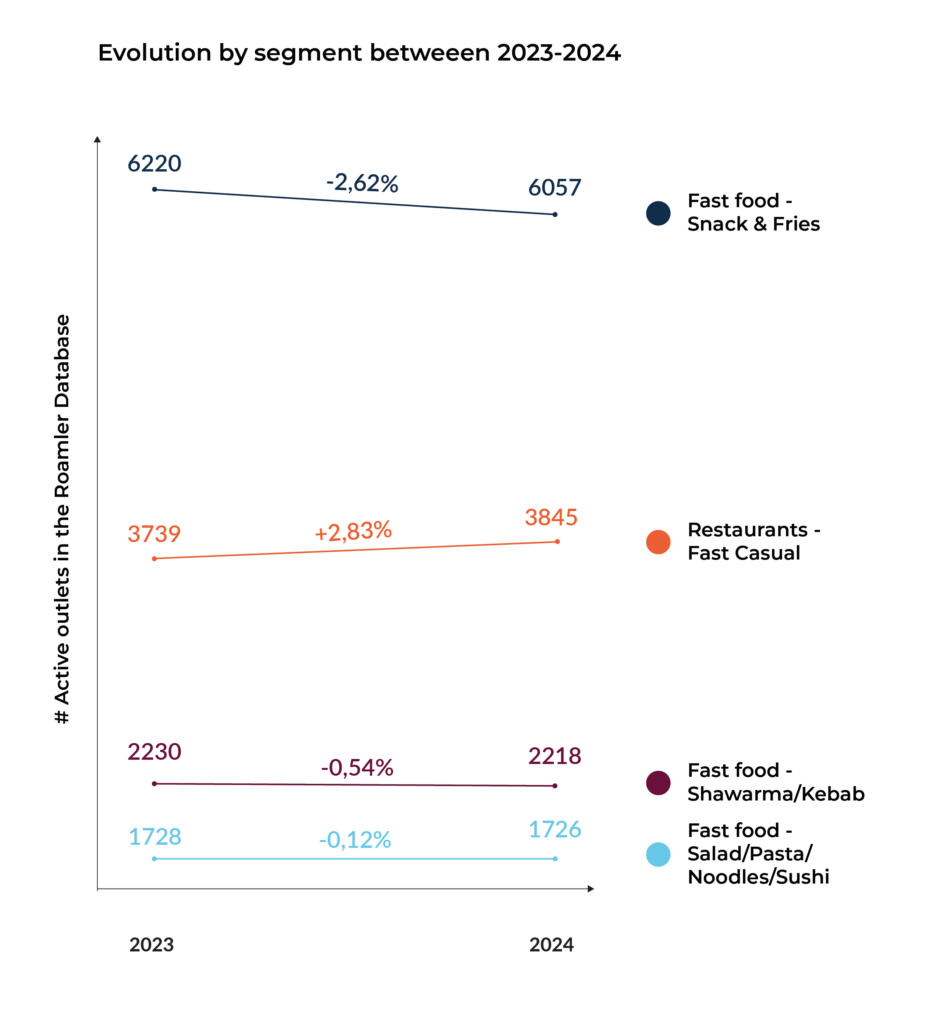

However, recent data suggests a shift, with a slight decrease in outlet numbers across several segments compared to the previous year. If we zoom on the years 2023 – 2024, we see a decline in outlet numbers for three out of the four segments, particularly noticeable in snack bars (-2,62%).

This decline compared to last year is consistent across other segments as well. Almost all dining/drinking establishments are experiencing a similar decrease compared to last year.

Roamler newsletter

Get the latest insights, innovations, and opportunities when it comes to efficiency for your business.

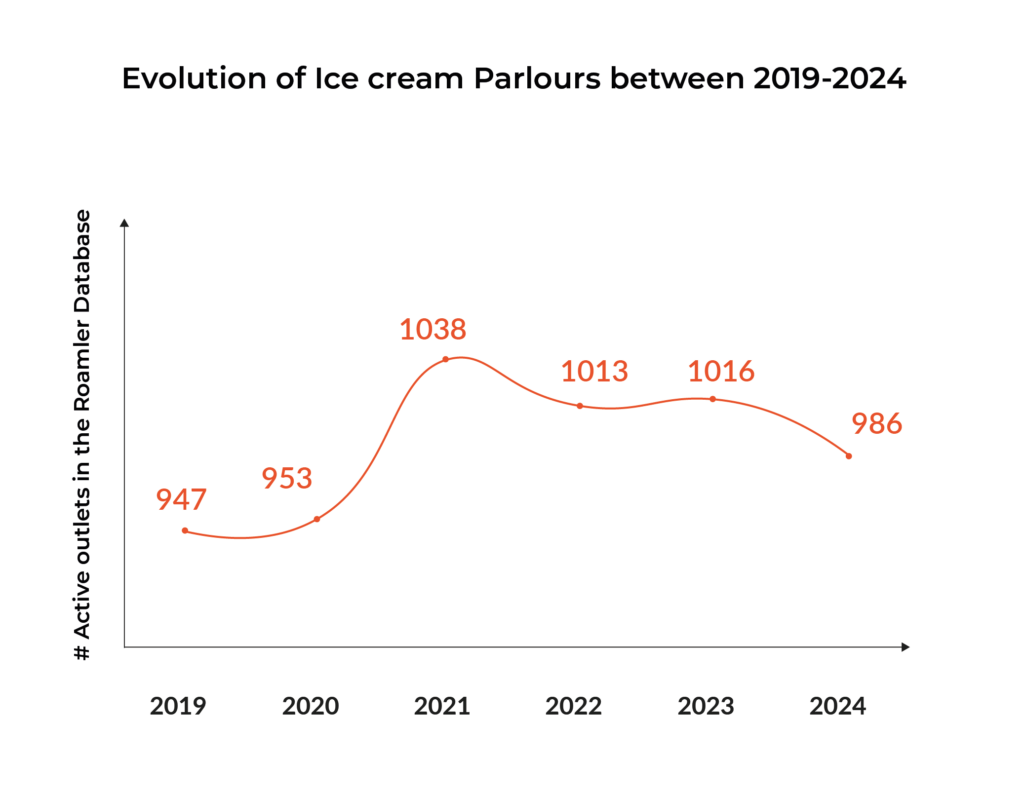

For some specific categories, the decline even occurred before 2023. This is the case for ice cream shops Ice cream Parlours. After an increase of 9,6% between 2019 and 2021, this category showed a decline of 5%.

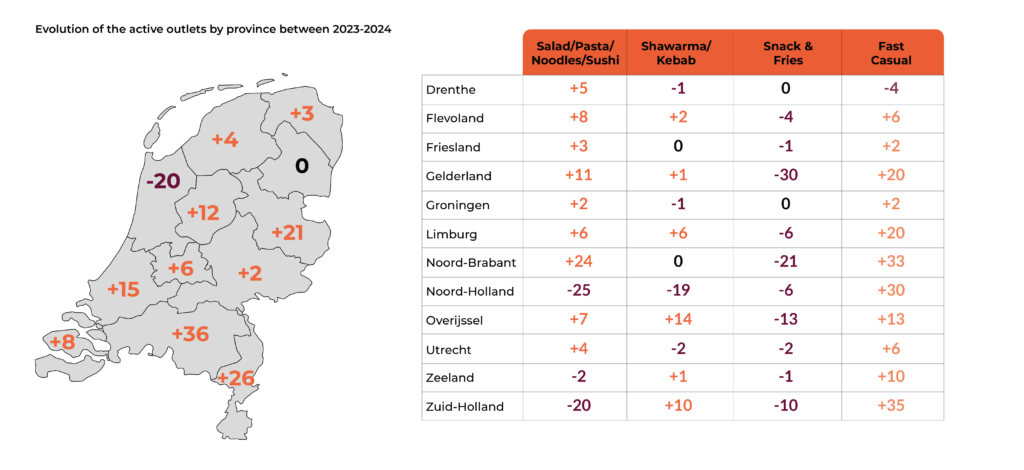

Overview by province

Analyzing the market regionally reveals interesting insights. North Holland, for instance, has witnessed a significant decline in outlets across all four segments, especially in the salad/pasta/noodles/sushi segment (-25 outlets). On the contrary, there has been a significant increase in North Brabant (+24 outlets.

Looking at the detailed number of outlets by provinces, we see that the Snack & Fries segment experienced a decrease in almost all provinces (especially in Gelderland, North Brabant, and Overijssel) between 2023 and 2024, which confirms the trend seen in part 1.

Another noteworthy insight is that fast-casual restaurants continues to grow steadily in all provinces of The Netherlands (except Drenthe). In a previous article, we have seen that since 2017, fast-casual restaurants have been growing at a much faster rate than the industry, at an average of over 10% year on year. In the last year, even if the segment is showing signs of slow down, it is still growing.

Insights from our Market Monitor

Insights sourced from our Market Monitor provide valuable data on brand performance and market share within the fast-service channel.

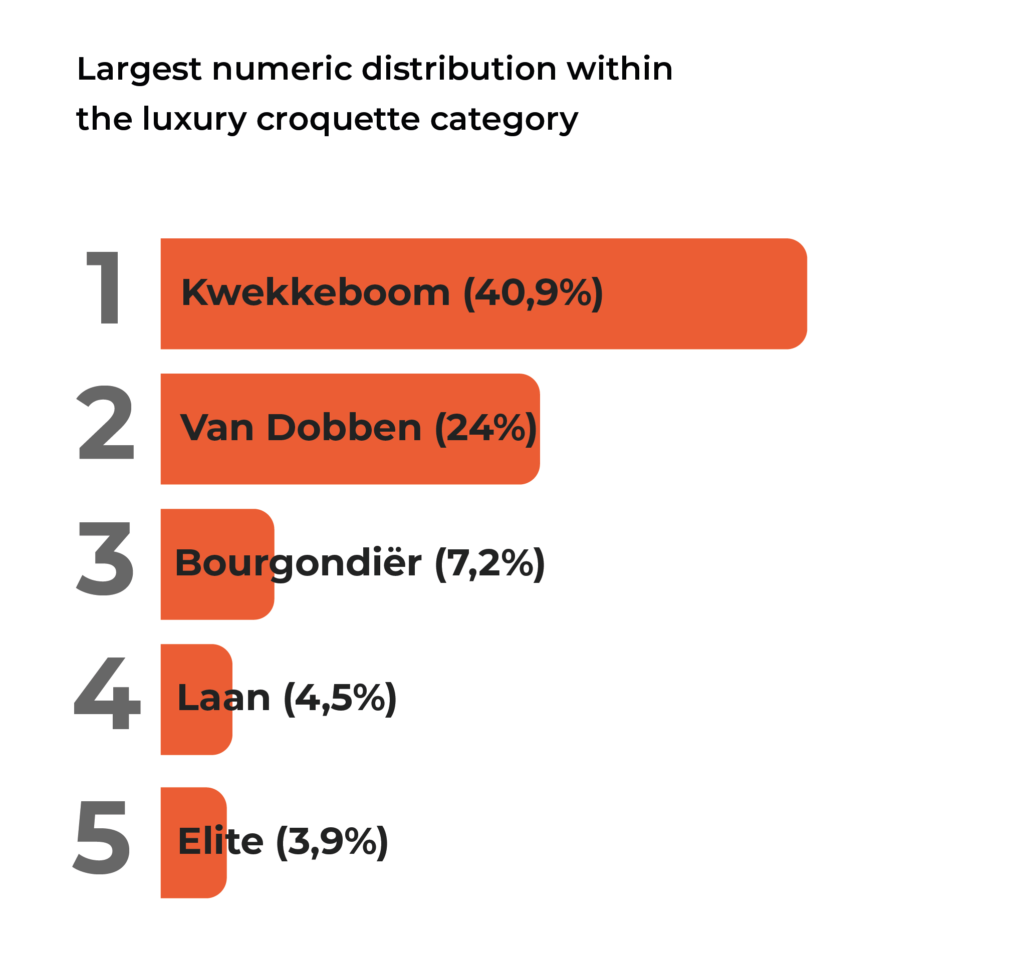

If we focus on numerical distribution within the luxury croquette category, we see that brands like Kwekkeboom and Van Dobben dominate the luxury croquette market with respectively 40,9% and 24%.

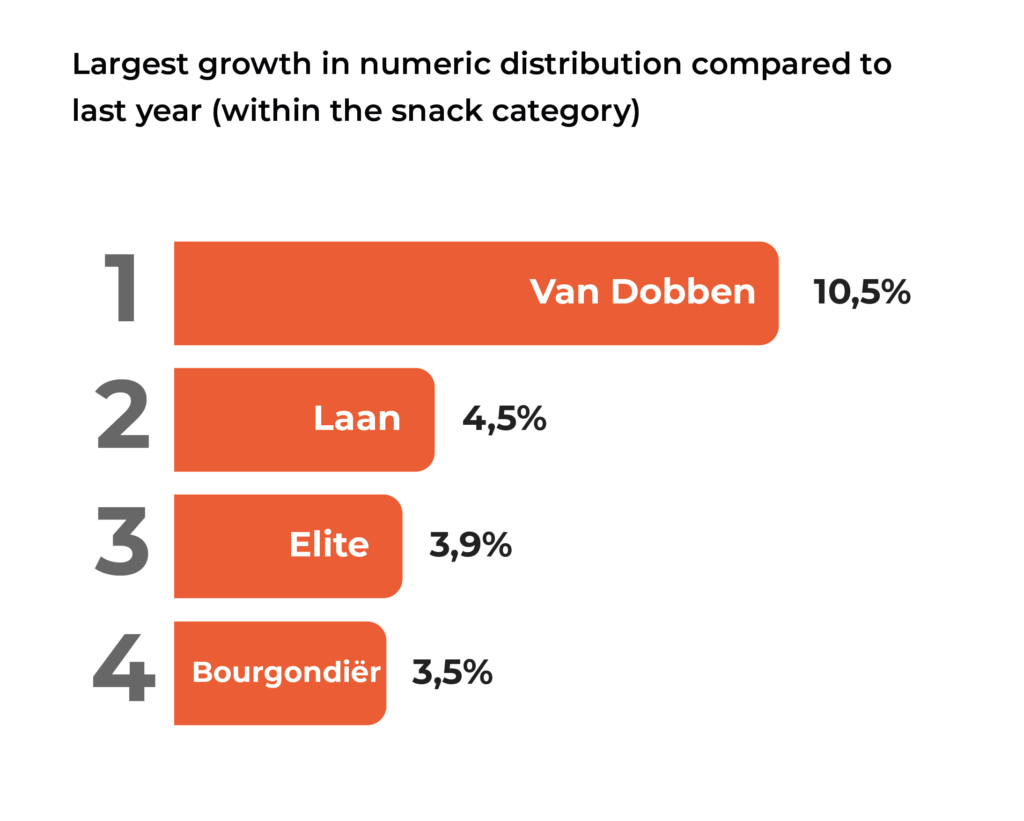

If we now focus on the growth in market share compared to last year, we see that Van Dobben has witnessed significant growth in market share (+10,5%) along with Laan, Elite, and Bourgondier.

Conclusion

The fast-service channel in the Netherlands is undergoing a period of transition. Snack bars and other fast-food locations are facing challenges, resulting in many closures, particularly in North Holland. On the other hand, fast-casual restaurant segment continues to grow rapidly.

Understanding the shifting dynamics of the Dutch fast-service market is now crucial to respond strategically and ensure growth. Did you know? Our Market Monitor gather data of approximately 8,000 fast-service locations in order to understand the market developments and gain valuable insights.

Access our Market Monitor, the most detailed continuous measurement across all channels of the out-of-home market