- Insights

Beer market in the Netherlands: a 2026 update

In 2024, we analysed the beer market in the Netherlands. Now, let’s take a look at how things have evolved in 2026. Using our out-of-home monitoring tool, we’ve explored key insights across bars/cafés and restaurants.

Which beer brands are the most popular?

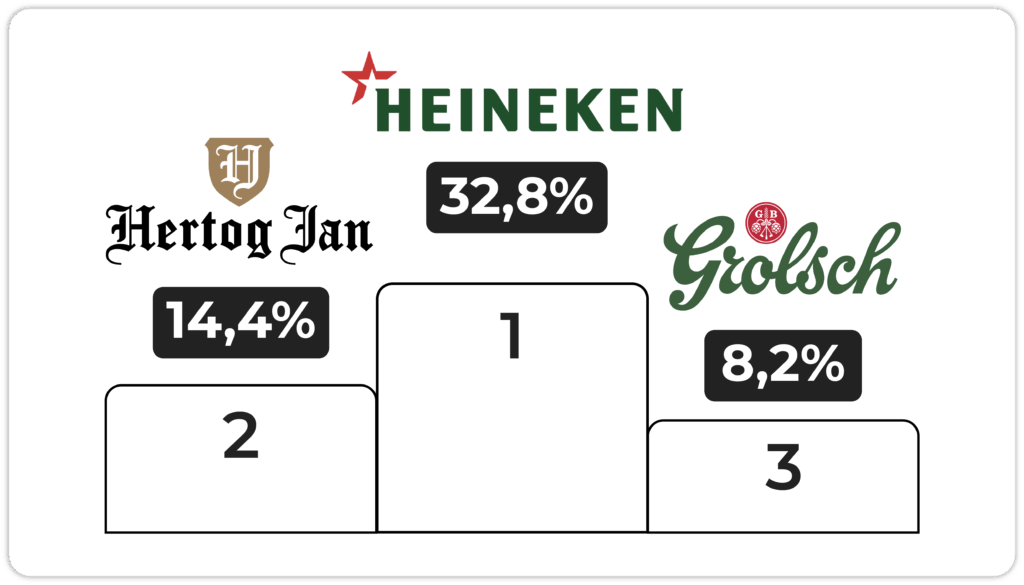

Since our last analysis, the leading beer brands in bars/cafés and restaurants have remained unchanged. Heineken (32.8% market distribution), Hertog Jan (14.4%), and Grolsch (8.2%) continue to dominate these segments.

In terms of presence, Heineken has further strengthened its position, gaining +3.2 percentage points compared to 2024. Its dominance is consistent across venue types: 36.0% in fast-casual restaurants, 34.1% in social dining, and 34.3% in bars, suggesting its strength comes from broad distribution rather than a particular segment affinity.

Meanwhile, Hertog Jan and Grolsch have seen slight declines in market distribution, at -0.6% and -0.8% respectively.

Regional differences across provinces

Of course, every province has its own preferences:

• In Limburg, Brand leads with 30.5% market distribution, while Heineken holds just 4.4%.

• In Noord-Brabant, Hertog Jan takes the lead at 23.2% with local rival Bavaria close behind at 18.2%.

• In Overijssel, Grolsch clearly dominates with an impressive 41.9%, its highest share across all provinces.

How is beer stored in venues?

A major evolution from our previous data is the focus on how beer is stored.

• Small kegs (<30L) remain the most common format, recorded in 42.3% of establishments, followed by bottles with 32.2%.

• Cellars are typically found in venues offering a wider beer selection. Establishments with a cellar have an average of 6.1 taps, compared to 3.6 taps for those without. These setups are more common in bars/cafés, which account for 40.4% of venues with a cellar — likely due to higher beer volumes compared to restaurants.

How many taps do venues have?

Most Bar/café and Restaurant locations have small tap setups: the most common configuration is 2-3 taps (26%), followed by 4-5 taps (24%). However, a significant tail of larger venues (20% with 6+ taps) pulls the overall up: on average, Dutch establishments have 4.2 taps.

Interestingly, venues serving Lindeboom or Gulpener as their main pilsner tend to offer a broader selection, with 5.1 to 5.3 taps on average. On the other hand, venues led by international brands like Veltins (3.1 taps) or Moretti (3.3 taps) usually have smaller setups, suggesting a more food-focused positioning where beer plays a secondary role.

Conclusion

The Dutch on-trade beer market continues to be shaped by strong national players, with a few notable regional exceptions. Heineken is further strengthening its position across the country, but local loyalty in regions like Limburg, Noord-Brabant, and Overijssel shows that even the market leader has its blind spots.

At the same time, the market is becoming increasingly split. Most venues still operate with compact setups of 2–3 taps and small kegs, while a growing share (around 20%) is investing in larger setups with 6+ taps and cellar systems. This creates different opportunities for brands, depending on the type of venues they choose to target.